Cost Segregation overview

Engineering-Appraisal-Based | IRS-Defensible | Institutionally Aligned

Cost segregation is a capital recovery strategy that reclassifies qualifying components of real property into shorter tax recovery lives, accelerating depreciation and improving early-period cash flow.

But cost segregation is not merely a tax exercise.

With us, cost segregation is practiced as a discipline of valuation economics and engineering-based asset classification, designed for assets where capital intensity, system complexity, and regulatory scrutiny materially affect recoverability.

We do not approach cost segregation as a template-driven reclassification service.

We approach it as capital recovery under uncertainty.

Cost Segregation as a Capital Recovery Discipline

In capital-intensive assets, depreciation outcomes are not driven by square footage — they are driven by:

- How systems are engineered

- How capital is deployed

- How assets are economically consumed

- How infrastructure supports production, power, and operations

Cost segregation, when properly executed, aligns tax recovery with economic reality, not architectural form.

This is particularly critical for:

- Infrastructure assets

- Power-intensive facilities

- Industrial and production-driven properties

- Data centers and energy systems

- Specialized commercial real estate

Our Engineering + Appraisal-Based Approach

Unlike generic or software-driven studies, our engagements integrate:

Engineering-Based Asset Identification

We analyze how systems are designed, installed, and function within the asset, including:

- Electrical and mechanical systems

- Process and production infrastructure

- Structural supports tied to equipment and systems

- Utility, power, and control architectures

Assets are classified based on economic function, not visual appearance or generic categories.

Appraisal-Based Capital Allocation

We apply appraisal discipline to:

- Reconstruct total project basis

- Abstract non-depreciable land using market and residual methods

- Reconcile all allocations internally

- Prevent distortions caused by improper shell or land allocation

This ensures depreciation outcomes reflect capital reality, not aggressive modeling.

IRS-Defensible, Audit-Ready by Design

Our studies are structured to withstand:

- IRS examination

- CPA and auditor review

- Transactional due diligence

- Institutional governance standards

Every engagement emphasizes:

- Transparent asset classification logic

- Engineering support for functional assignments

- Full reconciliation to total project cost

- Conservative interpretation aligned with IRS guidance

- Documentation suitable for Form 3115 and related filings

Acceleration is pursued only when supported by function, documentation, and law.

Bonus Depreciation: Why Methodology Matters More Than Ever

Recent federal legislation restored 100% bonus depreciation for qualifying property placed in service on or after January 20, 2025.

This allows qualifying 5-, 7-, and 15-year property to be fully expensed in Year 1 — for both new and used assets.

However, bonus depreciation is only as valuable as the quality of the underlying asset classification.

Template-based or aggressive studies can:

- Misclassify long-life property

- Over-allocate to qualifying classes

- Create IRS exposure

- Undermine audit defensibility

Our methodology ensures bonus depreciation is:

- Applied conservatively

- Technically supported

- Institutionally defensible

Cost Segregation by Asset Class

Our cost segregation practice is structured around infrastructure and capital intensity, not generic property categories:

Industrial & Manufacturing

Process-driven facilities with high utility and equipment integration

👉 [Industrial Cost Segregation]

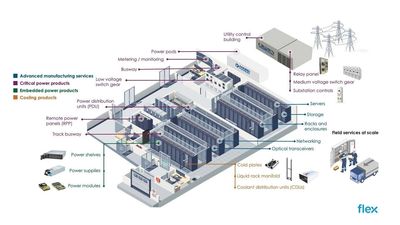

Data Centers

Power-dense, mission-critical infrastructure platforms

👉 [Data Center Cost Segregation]

Energy & Power Infrastructure

Nuclear, renewable energy, and power generation assets

👉 [Energy & Power Infrastructure Cost Segregation]

Commercial & Hospitality

Office, hotels, retail, mixed-use — executed with institutional discipline

👉 [Commercial & Hospitality Cost Segregation]

When Cost Segregation Is Most Valuable

- Upon placement in service

- At acquisition or recapitalization

- After expansion, retooling, or retrofit

- For multi-phase or campus-scale developments

- In connection with valuation, financing, or tax planning events

Bottom Line

Cost segregation, when properly executed, is not a tax strategy — it is a capital recovery discipline.

At US Valuation, cost segregation is:

- Engineering-informed

- Appraisal-disciplined

- IRS-defensible

- Designed for audit and institutional scrutiny

- Aligned with how infrastructure and commercial assets actually function

Begin with a Preliminary Review

We offer a no-fee preliminary feasibility discussion to assess whether a full study is appropriate and economically justified for your asset.

👉 Request a Preliminary Cost Segregation Review